U.S. President Donald Trump announced that he has decided on a candidate for the position of Chair of the Federal Reserve. It is no secret that the current Fed Chair, Jerome Powell, has displeased Trump by refusing to change the Fed's policy under pressure and by aggressively lowering interest rates.

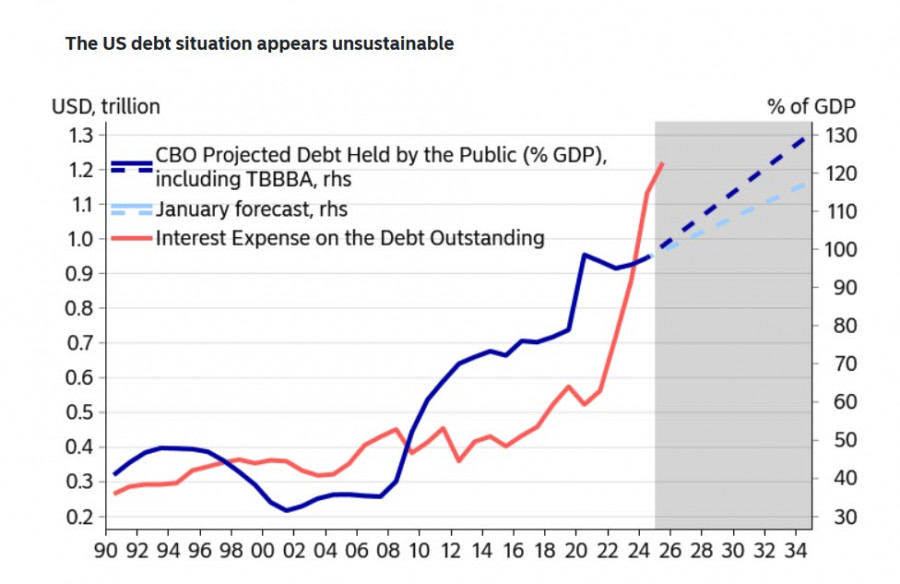

Trump knows what he is doing—high interest rates on bonds place an excessive burden on the budget. Interest payment expenses have sharply increased and already exceed defense spending, accounting for nearly 17% of the federal budget this year. The U.S. Congressional Budget Committee revised its debt forecast after passing the "big beautiful legislative bill," increasing it towards 2034 from January to nearly 129% of GDP, while the rate of growth in interest payments is currently significantly outpacing the growth of the debt.

Trump intends to reduce budget expenditures on interest payments and, therefore, demands aggressive rate cuts. However, if the inflation backdrop remains high and the Fed lowers rates, inflation expectations will not decline and may even rise, leaving bond yields at previous levels or causing them to increase. According to Nordea Bank, numerous factors indicate that U.S. Treasury yields will be higher in the coming years, and the need for borrowing will increase significantly. All of this jeopardizes the possibility of reaching a long-term agreement between Republicans and Democrats regarding the level of debt, and the dollar will not be supported by relatively high bond yields due to rapidly rising hedging costs.

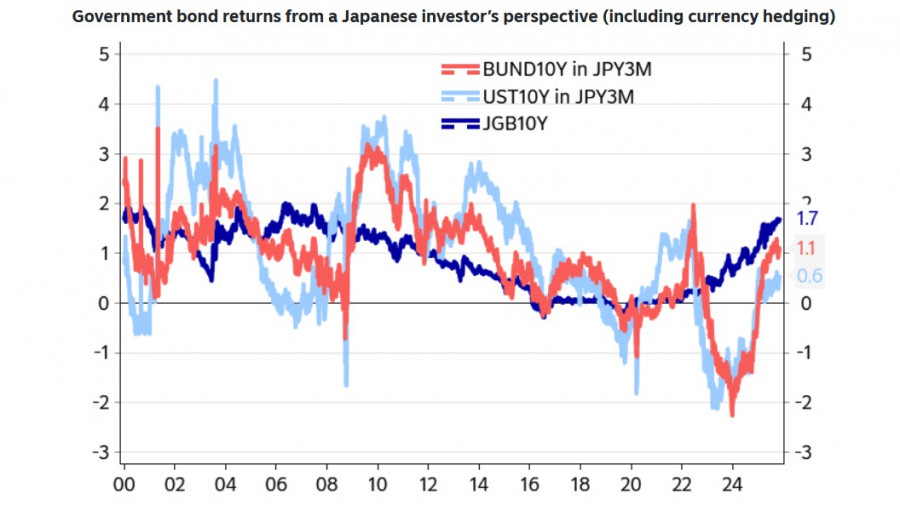

A high rate level may seem attractive to investors at first glance, but this situation is deceptive. Large investors typically hedge their risks, and when hedging costs are subtracted from yields, investments in U.S. Treasuries may appear less attractive to, for example, Japanese investors (the largest foreign holders of U.S. government debt) than investments in Japanese or even European securities.

Under these circumstances, the likelihood of the dollar strengthening in the short term is decreasing. Fed fund futures indicate a near 90% probability of an interest rate cut on December 10, with three more cuts expected next year. If Trump succeeds in replacing Powell as Fed Chair with one of his supporters, the likelihood of more aggressive rate cuts will increase even further. There is simply no other way to close the aggressively growing budget gap, especially since revenues from high tariffs are now being funneled into entirely different goals, namely sustaining consumer demand. Essentially, this means supporting inflation.

There are also other factors favoring a weak dollar. These are indirect but yield a powerful cumulative effect. Gold is resuming its rise after a month of consolidation, the Japanese yen strengthened sharply on Monday amid rumors that the Bank of Japan is indeed ready to raise rates in December, and the Chinese yuan reached a 14-month high against the dollar. The labor market is stagnating, and forecasts for U.S. GDP growth are deteriorating.

The upcoming week will provide much new information—ISM reports for November, ADP employment data in the private sector, import and export price dynamics, weekly unemployment claims, job cuts index, and the PCE price index for personal consumption, which the Fed considers in its decisions. We expect increased volatility and a gradual decline in the dollar against major currencies.

コンタクトする

コンタクトする