While market participants continue to assess the real prospects of a U.S. "takeover" of Europe and its economy, believing that any certainty is better than none, attention is shifting toward the start of the two-day Federal Reserve meeting on monetary policy, which begins today.

So, what is expected from the Fed's July meeting?

According to the consensus forecast, the Fed is expected to leave all parameters of its monetary policy unchanged. The key interest rate is expected to remain at 4.50%. Investors are not counting on any real possibility of a rate cut. Previously, despite comments from some central bank officials expressing openness to lowering rates, Chair Jerome Powell firmly defended the view that lowering borrowing costs was not advisable given the uncertainty surrounding the U.S. economy under the pressure of trade wars.

However, now that the U.S. has achieved breakthrough trade terms with Japan—and especially with the EU—the market may begin to expect Powell to soften his stance on rates. If, during tomorrow's press conference after the meeting, he even slightly hints at such a possibility, it would be a strong signal for the U.S. stock market and fuel expectations for a rate cut as early as the September meeting.

An additional positive factor could be the preliminary Q2 GDP data set, which is expected to be released before the meeting concludes. It is expected to show a significant increase to 2.4%, compared to a -0.5% contraction in the previous period. This news would also boost demand for equities and contribute to a generally upbeat market sentiment.

As for today's release of key economic data, the main focus will be on the JOLTS job openings report. The number of openings is projected to decline in June to 7.510 million from May's 7.769 million.

How might the market react to this data?

I believe the decline will not be seen as anything extraordinary or negative, as the market's focus remains on Trump's victories in the trade wars with Japan and the EU, along with the upcoming Fed meeting.

What can be expected in the markets today?

I believe Trump's victory in the tariff dispute with the EU will negatively impact the EUR/USD pair, as the EU's clearly losing position in trade with the U.S. will weaken the Continental European economy—and, through it, the euro. Previous hopes that the enormous sums allocated to European defense and German economic support would be offset are now being eroded by the "suzerainty rent" Europe will pay the U.S. in the form of a 15% tariff, commitments to purchase hundreds of billions of dollars' worth of weapons, and significant investments to support the U.S. economy.

In anticipation of the Fed meeting results, equity markets—especially in the U.S.—will likely be supported by hopes that the Fed may signal the possibility of a first rate cut this year in September.

Overall, I view the market outlook as positive.

The pair has broken out of the 1.1585–1.1800 range, increasing the likelihood of a further decline toward 1.1455. A potential sell level is 1.1554.

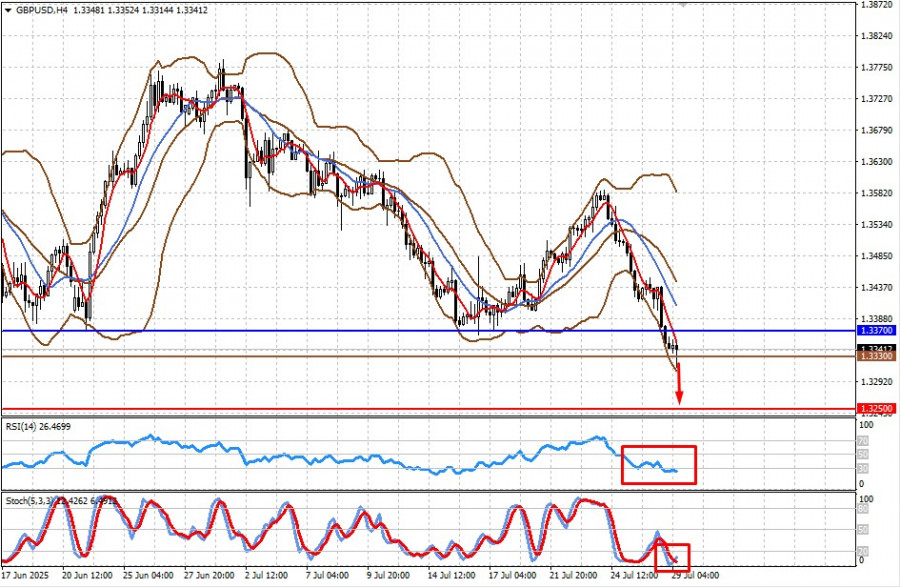

The pair remains under pressure from local UK-related negative factors, as well as the prospect of a further decline in EUR/USD. Against this backdrop, the pair may fall toward 1.3250. A potential sell level is 1.3330.

QUICK LINKS

Contact Us

Contact Us