US stock futures showed slight gains after Monday's selloff driven by the tech sector, as traders seized the opportunity to buy heavily discounted assets. This approach, often referred to as buying the dip, reflects market participants' confidence in long-term growth prospects.

Despite recent fluctuations, analysts note that fundamental indicators remain strong. Many companies continue to report stable earnings and growth, which supports demand for stocks and futures. Traders are also closely monitoring economic data that could influence the Federal Reserve's future policy. A significant batch of statistics is expected today, potentially affecting tomorrow's decision on interest rates.

However, risks of renewed market pressure remain, which could amplify Monday's selloff in the fintech sector. Traders are advised to exercise caution and stay vigilant.

S&P 500 futures rose 0.4%, and Nasdaq 100 contracts gained 0.7% before the regular session opened, following a 3% drop on Monday. Nvidia Corp. jumped 5% in premarket trading after plunging 17% the previous day. Broadcom Inc. and Marvell Technology Inc. also rose. Constellation Energy Corp., which supports energy-intensive AI data centers, climbed 4.7% after a 21% drop yesterday.

Meanwhile, the US dollar strengthened against major currencies, while copper prices fell following comments by President Donald Trump on tariffs provided Monday evening. Trump stated his intent to impose comprehensive tariffs far exceeding the 2.5% proposed by the Treasury Secretary. Speaking in Florida, he also promised to target specific sectors, including semiconductors, pharmaceuticals, steel, copper, and aluminum.

As mentioned earlier, many traders remain bullish in the stock market, viewing the current decline as an opportunity to buy. Notably, the Trump administration's discussions on new tariffs throughout January have yet to result in implementation, sustaining demand for risk assets. Trump's advisors have considered gradually increasing tariffs by 2–5% monthly.

Treasury yields edged lower, with the 10-year yield rising by two basis points to 4.55%.

This week, traders are focused on earnings announcements from companies like Microsoft Corp. and Apple Inc., expected later this week. Forecasts suggest that earnings growth for major tech firms this season will be the slowest in the past two years.

Corporate Reports

According to a published memorandum, HSBC will scale back parts of its investment banking operations in Europe, the UK, and the US. The largest banking group in Europe plans to exit equity capital markets and advisory services outside its core operations in Asia and the Middle East in the coming months.

SAP SE shares hit a record high. Europe's largest tech company reported fourth-quarter cloud sales slightly exceeding analysts' expectations, thanks to new AI-driven offerings attracting customers.

Shares of Siemens Energy AG rose as much as 5.1% in early trading. The company raised its full-year revenue outlook after surpassing analysts' projections for first-quarter revenue and profit.

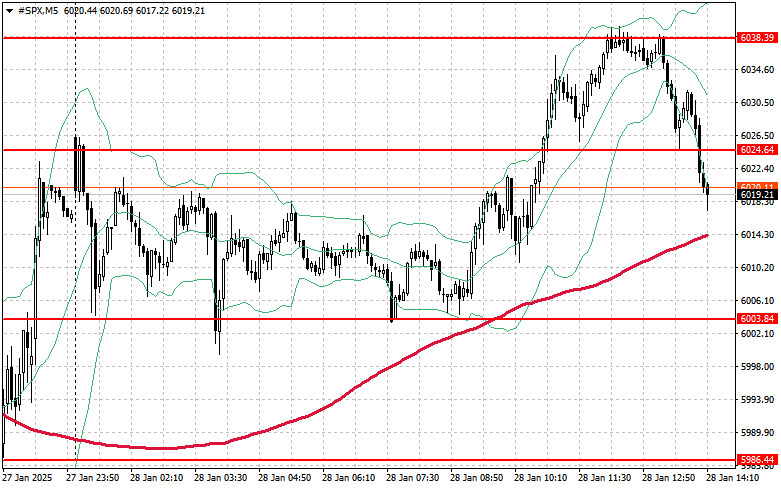

Demand remains strong for the S&P 500. Today, buyers may aim to break through the nearest resistance at $6,024, which would support the ongoing upward trend and pave the way for a push toward $6,038. Another key goal for bulls will be to maintain control above $6,047, solidifying buyers' positions. If demand for risk appetite declines and the market moves downward, buyers will need to step in around $6,003. A break below this level could push the index back to $5,986, allowing a decline toward $5,967.

RÁPIDOS ENLACES

Contáctenos

Contáctenos