The U.S. stock index S&P 500 ended Wednesday's trading session nearly unchanged as tech stocks managed to gain, but investors remained cautious due to geopolitical risks in the Middle East and anticipation of critical U.S. employment data expected later this week.

A rise in Nvidia shares by 1.6% provided support to the S&P 500's tech sector. However, Tesla shares declined by 3.5% after the electric vehicle manufacturer reported quarterly vehicle deliveries that fell short of market expectations.

Investors closely monitored developments in the Middle East after Israel vowed to retaliate for Iran's missile attack on Tuesday. U.S. President Joe Biden stated on Wednesday that he would not back an Israeli strike on Iran's nuclear facilities in response to the attack and urged Israel to act "proportionately."

Early Wednesday, data showed that U.S. private sector jobs increased more than expected in September, suggesting continued strength in the labor market. Still, traders remain focused on the upcoming non-farm payrolls report due Friday, as well as Thursday's jobless claims data, which could further influence market expectations.

With the market in a state of suspense, any surprise data or geopolitical developments could serve as a catalyst for volatility in the days ahead.

U.S. stock indices saw little change on Wednesday as investors prepared for an upcoming wave of earnings reports and Federal Reserve decisions. "We're about to see the employment report on Friday, and then next week kicks off the earnings season," commented Michael O'Rourke, Chief Market Strategist at JonesTrading in Stamford, Connecticut.

The Dow Jones Industrial Average added 39.55 points, or 0.09%, to close at 42,196.52. The S&P 500 edged up 0.01%, gaining just 0.79 points to end at 5,709.54. Meanwhile, the Nasdaq Composite rose by 14.76 points, or 0.08%, to 17,925.12.

The stock market wrapped up September with strong gains after the Federal Reserve unexpectedly cut rates by 50 basis points to support the labor market. As a result, the S&P 500 climbed 19.7% year-to-date.

The probability of another 25 basis point cut at the November FOMC meeting now stands at 65.7%, up from 42.6% a week earlier, according to the CME Group FedWatch tool.

JPMorgan Chase and other banking giants will kick off the third-quarter earnings season on October 11, setting the tone for the broader S&P 500 as investors look for signs of stability amid economic uncertainty.

Meanwhile, a strike involving 45,000 dockworkers, which has brought shipping at East Coast and Gulf Coast ports to a halt, entered its second day on Wednesday. Negotiations between the unions and employers have yet to be scheduled, according to sources.

Analysts at JPMorgan estimate that the strike is costing the U.S. economy approximately $5 billion per day, intensifying concerns over potential supply chain disruptions.

The market remains on edge as investors await further updates that could impact corporate earnings and broader economic trends.

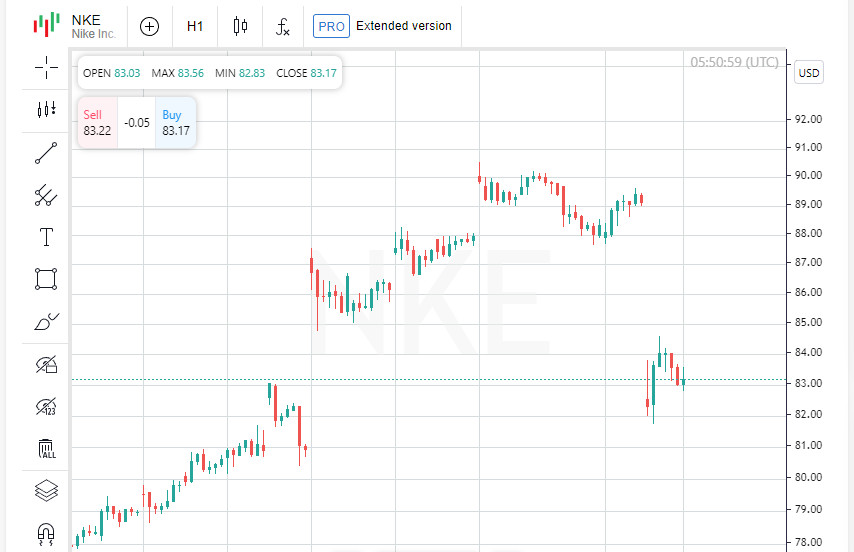

Nike shares dropped sharply by 7% on Wednesday after the sportswear giant pulled its annual revenue target, leaving investors puzzled over the company's turnaround timeline under new CEO Elliott Hill.

In addition to retracting its revenue forecast, Nike also canceled its investor day scheduled for November 19. The company's CFO, Matthew Friend, explained that the decision would provide Hill with "the necessary flexibility to review Nike's strategies and business trends," hinting at possible restructuring.

Currently, Nike's forward price-to-earnings ratio stands at 27.98, compared to 27.08 for Deckers and 35.14 for Adidas. Despite the recent decline, Nike shares, trading at $82, have still recovered 10% since the announcement of Hill's appointment in September.

The CEO of British retailer JD Sports expressed confidence in Hill, stating, "It's good to have someone from within the industry who knows Nike and understands its product range." This suggests that Hill's familiarity with the company could help navigate Nike through its current challenges.

Other sportswear stocks weren't immune to the market's jitters: Under Armour and Lululemon both declined by over 2%, while Foot Locker fell by 3%, reflecting broader concerns about supply chain disruptions and sales slowdowns.

Elsewhere, shares of Humana Inc. tumbled 11.8% after the health insurer warned that it expects a drop in enrollment in its top-rated Medicare Advantage plans for seniors in 2025. This statement has sparked worries about the broader healthcare sector's outlook.

With markets digesting these developments, Nike's outlook remains under scrutiny as the company grapples with uncertain forecasts and growing competition.

Global markets displayed mixed performance as traders digested U.S. labor data and awaited signals from the Federal Reserve. "Given the latest job numbers in the private sector, the bond market is betting against a 50 basis point cut at the next Fed meeting," noted Matt Miskin, Co-Chief Investment Strategist at John Hancock Investment Management.

The MSCI global equity index (MIWD00000PUS) dipped by 0.04% to 845.49 points, reflecting overall cautious sentiment. Earlier, the STOXX Europe 600 managed to close with a slight gain of 0.05% at 521.14 points.

On the energy front, U.S. crude oil rose 0.39% to $70.10 per barrel, while Brent finished the day at $73.90 per barrel, up 0.46%. Despite geopolitical tensions in the Middle East, the upward momentum was capped by a significant increase in U.S. crude inventories.

U.S. Treasury yields continued their upward trajectory: the benchmark 10-year yield climbed by 4 basis points to 3.783%, compared to 3.743% the previous day. Meanwhile, 30-year bonds saw a 4.9 basis point rise, closing at 4.1299%. The 2-year yield, which is more sensitive to Fed rate expectations, edged up 1.4 basis points to 3.6352%.

A closely-watched segment of the U.S. yield curve, measuring the gap between 2-year and 10-year yields, remained at a positive 14.6 basis points — suggesting that investors are not pricing in a near-term recession.

The dollar index, which tracks the greenback's value against a basket of currencies, rose by 0.34% to 101.60. The euro slipped by 0.16% to $1.1049, while the dollar surged 2% against the Japanese yen, reaching 146.43.

In the precious metals market, spot gold declined by 0.14% to $2,659.22 per ounce, while U.S. gold futures fell by 1.02% to $2,640.00. Rising bond yields and a stronger dollar weighed on gold's appeal as a safe-haven asset.

With traders balancing geopolitical risks and economic indicators, market sentiment remains fragile, and any new developments could tip the scales in unexpected directions.

فوری رابطے

ہم سے رابطہ کریں

ہم سے رابطہ کریں