The gold market is enduring one of the most dramatic declines of the last decade. Against the backdrop of a sharp price correction, investors and traders are searching for an explanation — and one was voiced as early as January. ARK Invest CEO Cathie Wood made a loud claim then: not artificial intelligence but gold is the most "overheated" asset in today's market. Her words now have a chilling confirmation.

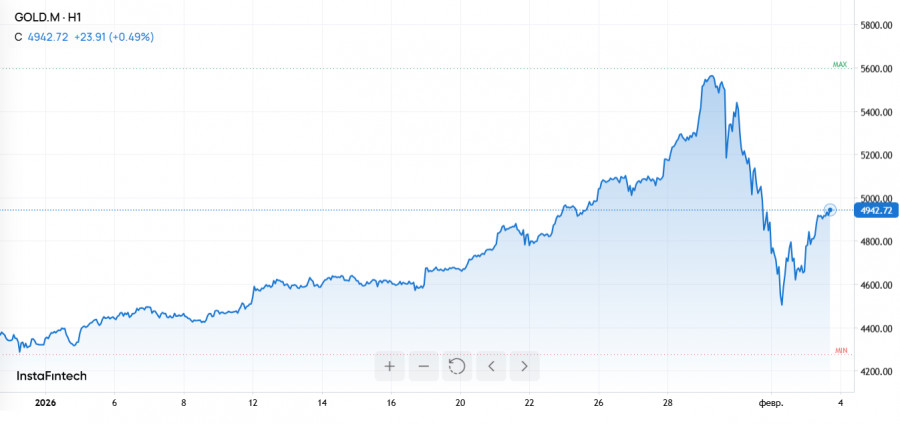

As of Monday, gold had slumped to $4,544 per ounce, losing more than $1,000 from its record high of $5,594.82 recorded on January 30. A particularly violent sell?off occurred on Friday: the price dropped nearly 10% in one session, the steepest single?day fall since 1983. Silver followed, plunging about 31% — its worst day since the Hunt brothers' crash in 1980.

Cathie Wood justified her warning by analyzing fundamentals. According to ARK Invest, gold's market capitalization now stands at about 170% of US M2 money supply — a historically high level last seen during the Great Depression in 1934 and slightly above the 1980 peak. Levels like these, Wood argues, signal speculative overheating.

"There is a high probability that gold is heading for a decline," Cathie Wood wrote on X in late January. "Parabolic rallies usually end with equally rapid collapses. In our view, the bubble today is not in AI, it's in gold."

Currency policy was also a catalyst. One trigger for the drop in precious?metal prices was a stronger dollar after President Donald Trump nominated Kevin Warsh as Fed chair — a figure associated with hawkish monetary policy. That nomination drove a sharp dollar rally, increasing pressure on gold.

Comparing today's situation with historical crises, Wood stressed that current economic realities differ significantly from the inflationary 1970s or the deflationary 1930s. Ten?year US Treasury yields, for example, have fallen from about 5% at the end of 2023 to around 4.2% — implying financial conditions are easing rather than tightening.

Supporting this view, Robin Brooks, former chief economist at the Institute of International Finance, noted that the recent gold rally was "largely driven by retail purchases" and was not accompanied by active central?bank buying — a picture corroborated by IMF data.

Still, market views are divided. Wood's influence on investor sentiment is considerable, but not everyone is ready to declare the multi?year gold bull market over. J.P. Morgan, for instance, forecasts gold could rise to $6,300 per ounce by year?end, while analysts at CMC Markets call the current drawdown "a normal correction after an impressive rally" and advise against treating it as a collapse.

For traders, the current price drop presents unique opportunities. Sharp volatility creates conditions for short?term short trades as well as for buying rebounds. Analyzing fundamental drivers such as Fed policy shifts and the dollar's path can help shape more precise strategies.

Finally, despite current pressure, long?term investors may view the correction as a chance to accumulate positions well below recent highs. Key, however, is prudent calculation and reliance on macro signals rather than emotion. That is the only way to separate market noise from real investment opportunities.

SZYBKIE LINKI

Skontaktuj się z ForexMart

Skontaktuj się z ForexMart