Silné výsledky, ale slabý vývoj ceny akcií

Akcie cloudové společnosti DigitalOcean v roce 2025 zatím ztratily na hodnotě přes 17 %, a to navzdory tomu, že firma zaznamenává lepší výsledky, než se očekávalo. Zklamání investorů tak působí poněkud nelogicky, zejména v kontextu výhledu na rekordní tržby.

Za první čtvrtletí roku 2025 DigitalOcean vykázal tržby ve výši 211 milionů dolarů, což znamená meziroční nárůst o 14 %. Očekávání Wall Street přitom byla mírně nižší – kolem 209 milionů dolarů. Představenstvo společnosti navíc věří, že za celý rok 2025 dosáhne tržeb až 890 milionů dolarů, což by byl další 14% růst oproti loňským 13 %.

Přesto jsou akcie DigitalOcean stále zhruba 80 % pod historickými maximy z roku 2021. Tento nepoměr mezi vývojem podnikání a oceněním může některé investory frustrovat, pro jiné ale znamená příležitost.

DigitalOcean dlouhodobě cílí na menší podniky a vývojáře, přičemž přibližně 400 000 zákazníků utrácí méně než 50 dolarů měsíčně. Tento segment je často přehlížen velkými poskytovateli cloudu, což umožňuje DigitalOcean růst mimo jejich přímý dosah.

V posledních letech ale společnost čelila tlaku – zákazníci v průměru utráceli méně, což se promítlo do metriky známé jako čistá míra retence v dolarech (NDR). Hodnota 100 % v prvním čtvrtletí 2025 znamená, že zákazníci utráceli stejně jako před rokem. Ačkoliv to není špatný výsledek, je potřeba dodat, že NDR byla pod 100 % již šest čtvrtletí v řadě, což je pro softwarovou firmu varovný signál.

Do této stagnace ale zasáhl nový faktor – umělá inteligence. DigitalOcean investoval do infrastruktury pro AI a výsledky na sebe nenechaly dlouho čekat. Roční opakované výnosy z AI vzrostly meziročně o více než 160 %, přičemž vedení uvádí, že „poptávka převyšuje nabídku“. Tento trend by mohl být pro firmu rozhodující.

Investice do AI nejsou levné. Budování výpočetních kapacit a datových center zvyšuje kapitálové výdaje rychleji než tržby. Přesto zůstává DigitalOcean ziskový, s volným peněžním tokem přes 70 milionů dolarů za posledních 12 měsíců.

Navíc je pravděpodobné, že velká část těchto výdajů se koncentrovala do prvního čtvrtletí, což otevírá prostor pro zlepšení ziskovosti ve zbytku roku 2025. Tato kombinace růstu, investic do budoucnosti a udržení ziskovosti je pro dlouhodobé investory příznivá.

Přesto existují rizika – být menším hráčem na trhu veřejného cloudu znamená čelit konkurenci a hledat neustálé inovace, aby si firma udržela zákazníky. Náklady na AI mohou nadále růst a tlak na marže přetrvávat. Ale právě tato fáze může být momentem, kdy se začíná formovat další růstový cyklus.

Zřejmě nejzajímavější aspekt příběhu DigitalOcean je diskrepance mezi výkonem firmy a oceněním akcií. Poměr ceny k tržbám (P/S) klesl na úroveň 3, přestože se pod vedením nového managementu zrychlil růst a zlepšila hrubá marže.

Jde o situaci, kdy podnik fundamentálně sílí, ale cena akcií na to nereaguje. Pokud se trendy v růstu a maržích potvrdí i v následujících čtvrtletích, může to přinést výrazné přecenění akcie směrem vzhůru. Trh zatím neoceňuje pokrok, který DigitalOcean učinil.

Investoři tak mají před sebou akcii, která sice nese určitá rizika, ale zároveň nabízí potenciál asymetrického výnosu – tedy vyšší možný zisk ve srovnání s relativně nízkou současnou cenou.

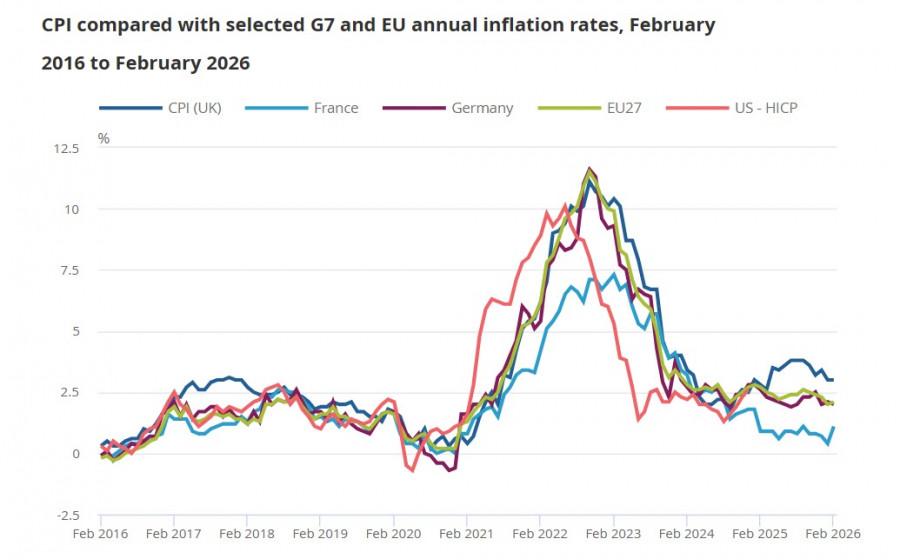

Inflation in the UK remained at 3% in February, which is now completely outdated, as it does not account for the price surge in March due to the energy market crisis. At the same time, even under these stable conditions, core inflation rose from 3.1% to 3.2%, which almost certainly indicates that all price components will grow in March.

Comparing price dynamics between the UK and EU countries, the overall price level at the beginning of March remained significantly higher in the UK. While ECB forecasts suggest a rate hike as early as April, the latest market expectations for the Bank of England imply three rate increases this year.

What does the war in the Middle East mean for the UK economy? It is clear that economic growth will slow down, which, in turn, will lead to a decrease in tax revenues – falling consumer spending reduces VAT income, struggling businesses lead to lower corporate tax revenues, and slowing wage growth suppresses future income from income tax. In the worst-case scenario, all of this will be compounded by rising unemployment, business closures, and increasing social welfare costs.

With GDP growth slowing, actions to ease financial conditions are in demand. But not in this case, as the rising inflation, which is inevitable, will lead to increasing interest rates. A feedback loop arises, from which it is difficult to exit, and if no action is taken, this scenario will lead to stagflation. But what to do – it remains unclear.

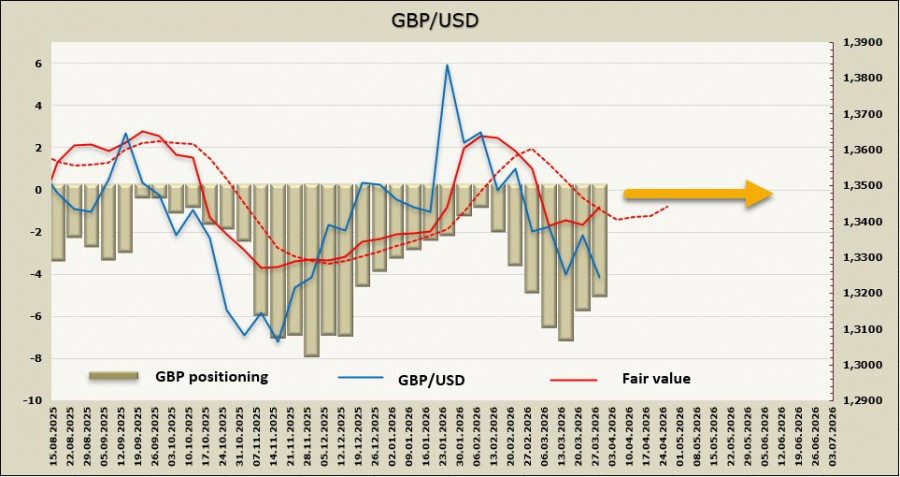

It is apparent that the Bank of England has completed its rate-cutting cycle and is ready to embark on a rate-hiking cycle, albeit reluctantly, which is a factor favoring the strengthening of the pound. All other factors point to a weakening, as capital will flow to those regions of the world that will suffer the least from the energy shock and can provide decent returns with minimal risks. The UK is not one of those regions, so in the long term, if the war drags on, the pound has little room to strengthen.

The net short position on GBP decreased by 0.6 billion over the reporting week to -4.9 billion, with positioning remaining bearish. The recalculated price, due to the bond correction following last week's failure, has returned to its long-term average, so the chances of continued growth are slim.

As we expected a week ago, after a brief correction, the pound headed down, updating its 3-month low. The target of 1.3000/50, which we previously saw as medium-term, is becoming increasingly closer. Unexpected news about a decrease in escalation in the Gulf could halt the decline, but the probability of such an event is diminishing. The market is gradually realizing that the crisis is not only not ending, but on the contrary, is acquiring increasingly global dimensions. A decline of the pound in the current conditions is the most likely scenario.

HIZLI BAĞLANTILAR

show error

Unable to load the requested language file: language/turkish/cookies_lang.php

date: 2026-03-31 02:54:11 IP: 172.18.0.1

Bize Ulaşın

Bize Ulaşın